© 2026 GEMP – German Egyptian Manufacturing & Procurement (GEMP Consulting).

What “nearshoring to Egypt” looks like in practice

Nearshoring rarely means moving everything out of Asia. In practice, it is often a second pillar: a regional plant (or manufacturing partner) that serves EU customers faster, absorbs volatility and provides redundancy. Common entry models include:

• Final assembly / late customization in Egypt

• Modules and sub‑assemblies (e.g., skids, panels, piping spools, steel structures)

• Dual sourcing: regionalize critical parts while keeping some global sourcing

The key mindset shift: nearshoring is best executed as supply‑chain architecture, not a pure “cost play.”

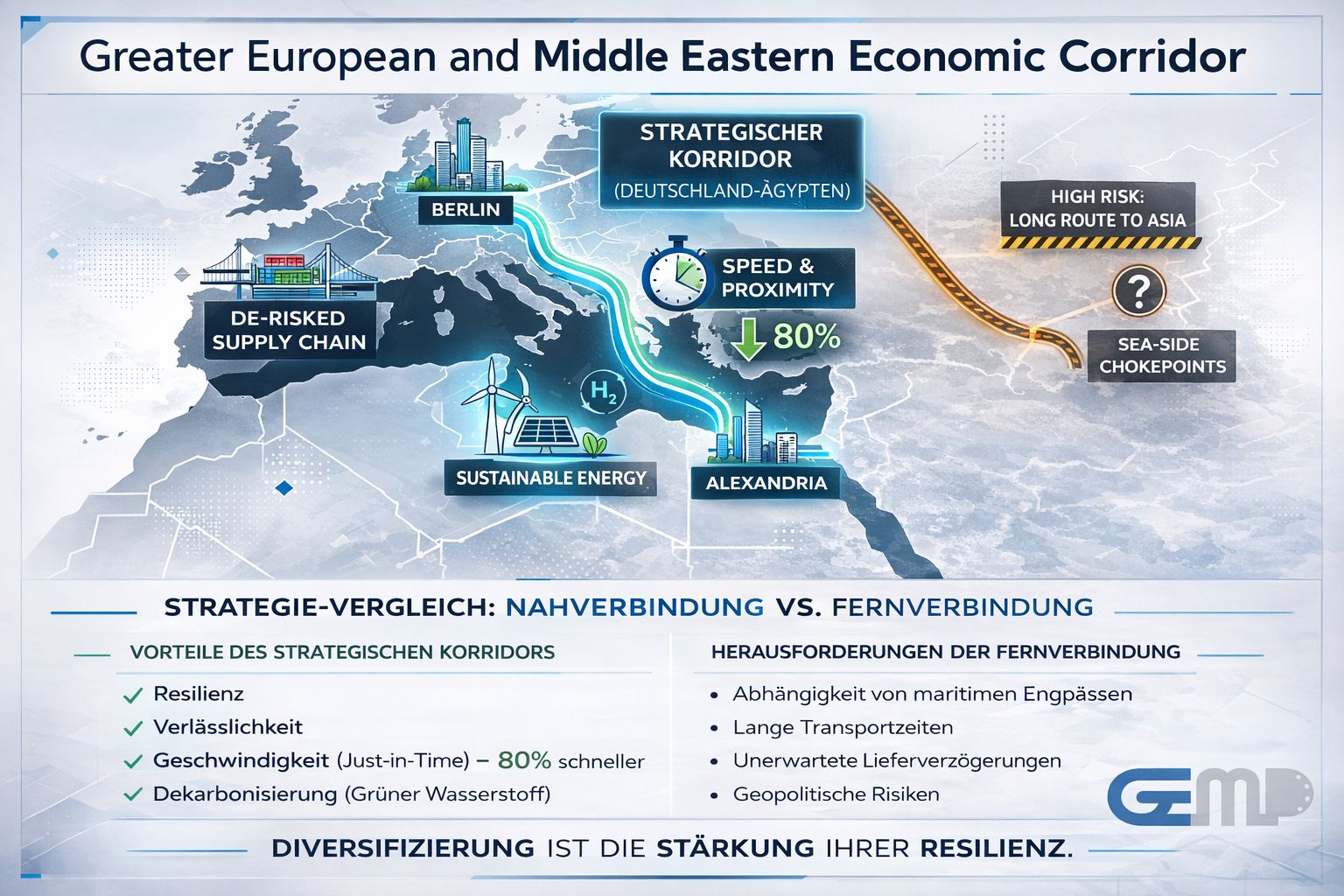

The advantages — and why Egypt is often “faster” than India and China for Europe

Advantage A: Shorter distance = faster reaction cycles

For EU‑focused volumes (spares, variants, smaller batches, volatile demand), proximity is a real competitive lever. Egypt’s distance to Europe is structurally shorter than India or China, reducing both transit time and, crucially, uncertainty. When the Red Sea route becomes constrained, Asia–Europe detours via Africa can add up to two weeks.

That “time buffer” turns into inventory, working capital and service‑level pressure.

Advantage B: Time zone and operational proximity

Egypt is typically only 1–2 hours away from Central Europe, which improves:

• live engineering/quality alignment

• faster escalation and approvals

• easier on‑site visits and audits than time‑zones 4–7 hours away (India/China)

This is especially valuable for engineered products, variants and regulated industries.

Advantage C: EU market access and rules‑of‑origin frameworks

Trade frameworks can become a decisive differentiator:

• The EU–Egypt Association Agreement has been in force since 2004 and creates a free‑trade area, including the removal of tariffs on industrial products.

• Egypt is part of the Pan‑Euro‑Med (PEM) origin / cumulation system, relevant when supply chains span multiple PEM partners.

• For certain products, QIZ can enable duty‑free access to the US (product‑ and rule‑dependent).

India: The EU Commission states EU–India FTA negotiations were concluded in January 2026 — but practical application typically depends on subsequent implementation steps.

China: An EU Commission Q&A notes there is no Council authorisation to negotiate a trade agreement with China (in the CAI context).

Advantage D: Logistics and industrial infrastructure is being expanded

Egypt’s Suez corridor is not just about transit; it is increasingly about industrial capability. The Suez Canal Economic Zone (SCZONE) highlights investment rules, incentives and trade connectivity.

In parallel, a major rail axis is being built and publicly referenced as “Suez Canal on Rails”: a “Green Line” is planned to connect Cairo with Ain Sokhna (Red Sea) and Alexandria (Mediterranean).

That supports a practical “land bridge” concept between Red Sea and Mediterranean logistics.

Advantage E: Free‑zone models for import‑process‑re‑export

For many manufacturing setups, Egypt’s Free Zone frameworks matter — describing customs/tax exemptions for imports and exports under Free‑Zone rules (with defined treatment if goods enter the domestic market).

Egypt vs India vs China — an honest decision‑maker comparison

China still leads many sectors on supplier depth and scale. India offers growth, talent and a large domestic market. Egypt often wins not by “being best at everything,” but by being a high‑control, fast‑to‑Europe complement.

Egypt wins when EU demand is dominant, lead time and variants matter, and rules‑of‑origin/tariff integration is key.

India wins when the India market is part of the strategy and large‑scale capacity is the priority (and future EU–India trade terms are operational).

China wins when maximum ecosystem depth and scale outweigh longer lead times and higher geopolitical/trade complexity.

Risks — and how to manage them

Risk 1: High dependency on imported inputs

If most inputs still come from Asia, you remain partially exposed to the Suez/Red‑Sea risk. Detours can add weeks.

Mitigation: build regional supplier depth for top A‑parts; redesign inventory buffers; qualify alternative carriers/routes.

Risk 2: Customs, compliance and operational set‑up

Nearshoring succeeds or fails on the import/export design (Free Zone vs onshore, VAT/customs, brokers, documentation).

Mitigation: design the goods flow up front and document it for auditability.

Risk 3: Quality and supplier development

Supplier depth can be lower than in China for certain categories.

Mitigation: pilot phase, supplier qualification, robust QA/traceability and dual sourcing.

Risk 4: Regional perception and route volatility

Boards may bundle “region risk” together even when specific site risk differs.

Mitigation: separate location risk from shipping‑route risk; build BCP/insurance/security concepts.

Risk 5: No clear target model

If the goal is only “cheaper,” execution often fails.

Mitigation: prioritize objectives (speed, resilience, tariff/origin, CO₂, service) and choose the operating model accordingly.

A pragmatic roadmap for decision‑makers

Start with the products where speed and variability are expensive. Build a pilot, lock quality, then scale — and only then push deeper localization.

Sources:

EU–Egypt Association Agreement (Access2Markets):

https://trade.ec.europa.eu/access-to-markets/en/content/eu-egypt-association-agreement

EU trade relations with Egypt (EU trade policy site):

https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/egypt_en

Pan-Euro-Mediterranean (PEM) cumulation & PEM Convention (European Commission):

https://taxation-customs.ec.europa.eu/customs/international-affairs/pan-euro-mediterranean-cumulation-and-pem-convention_en

Pan-Euro-Mediterranean Convention (Access2Markets):

https://trade.ec.europa.eu/access-to-markets/en/content/pan-euro-mediterranean-convention-pem

Qualifying Industrial Zones (QIZ) – Egypt (International Trade Administration, U.S. Dept. of Commerce):

https://www.trade.gov/qiz-egypt

Suez Canal Economic Zone (SCZONE – official):

https://sczone.eg/

Free Zones – Egypt (GAFI overview page):

https://www.gafi.gov.eg/English/StartaBusiness/InvestmentZones/Pages/FreeZones.aspx

Private Free Zones in Egypt (GAFI PDF):

https://www.gafi.gov.eg/English/StartaBusiness/InvestmentZones/PublishingImages/Pages/FreeZones/En_Pri_all_final.pdf

Siemens press release on “Green Line” linking Cairo with Ain Sokhna & Alexandria (“Suez Canal on Rails”):

https://press.siemens.com/global/en/pressrelease/siemens-unveils-velaro-high-speed-train-transmea-2025-cairo

Electric High-Speed Rail Project – Ain Sokhna (Red Sea) to Alexandria (Mediterranean) (Egypt SIS):

https://sis.gov.eg/en/projects-initiatives/projects/electric-high-speed-rail-project/

EU–India trade agreement (European Commission – negotiations concluded Jan 2026):

https://commission.europa.eu/topics/trade/eu-india-trade-agreement_en

EU trade relations with India (EU trade policy site):

https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/india_en

EU Commission Q&A on EU–China CAI (includes note on no mandate for an EU–China trade agreement):

https://ec.europa.eu/commission/presscorner/detail/pl/qanda_20_2543

Red Sea situation & shipping impact (DHL Global Forwarding):

https://www.dhl.com/eg-en/home/global-forwarding/latest-news-and-webinars/red-sea-situation-impact-shipping.html

Example reporting: rerouting around Africa due to Red Sea constraints (Reuters, 27 Feb 2026):

https://www.reuters.com/world/middle-east/maersk-reroutes-some-sailings-around-africa-due-unforeseen-constraints-in-red-2026-02-27/

Example reporting: “adding up to two weeks” transit time (Lloyd’s List, 10 Jan 2024):

https://www.lloydslist.com/LL1147882/Vehicle-carrier-operators-divided-over-Suez-route-as-more-ships-divert-via-South-Africa

David Weber

David Weber